Most people buy an extended car warranty thinking it’s a safety net for big repairs. But if you don’t know what’s excluded, you could be left paying thousands out of pocket when you need it most. Nearly 60% of car owners don’t read the fine print - and that’s where the trouble starts.

What You Think Is Covered (But Isn’t)

You paid extra for peace of mind, right? So when your transmission goes out at 140,000 miles, you expect the warranty to cover it. But what about the brake pads that wore out six months later? Or the cracked dashboard from years of sun exposure? Those won’t be covered - and most buyers never realize it until they’re at the repair shop with a $1,200 bill.Routine Maintenance Is Never Covered

This is the biggest surprise for most people. An extended warranty doesn’t pay for oil changes, air filters, spark plugs, wiper blades, or tire rotations. These are normal upkeep items - not failures. Even if your car is under warranty, you still need to budget for these every 5,000 to 7,500 miles. Some companies like Endurance offer optional maintenance allowances, but those are add-ons, not the base plan.Wear-and-Tear Parts Are Out

Parts designed to wear out over time are almost always excluded. That includes:- Brake pads and rotors

- Clutch assemblies

- Alternators

- Headlight and taillight bulbs

- Belts and hoses

- Tires

Pre-Existing Damage Is a Hard No

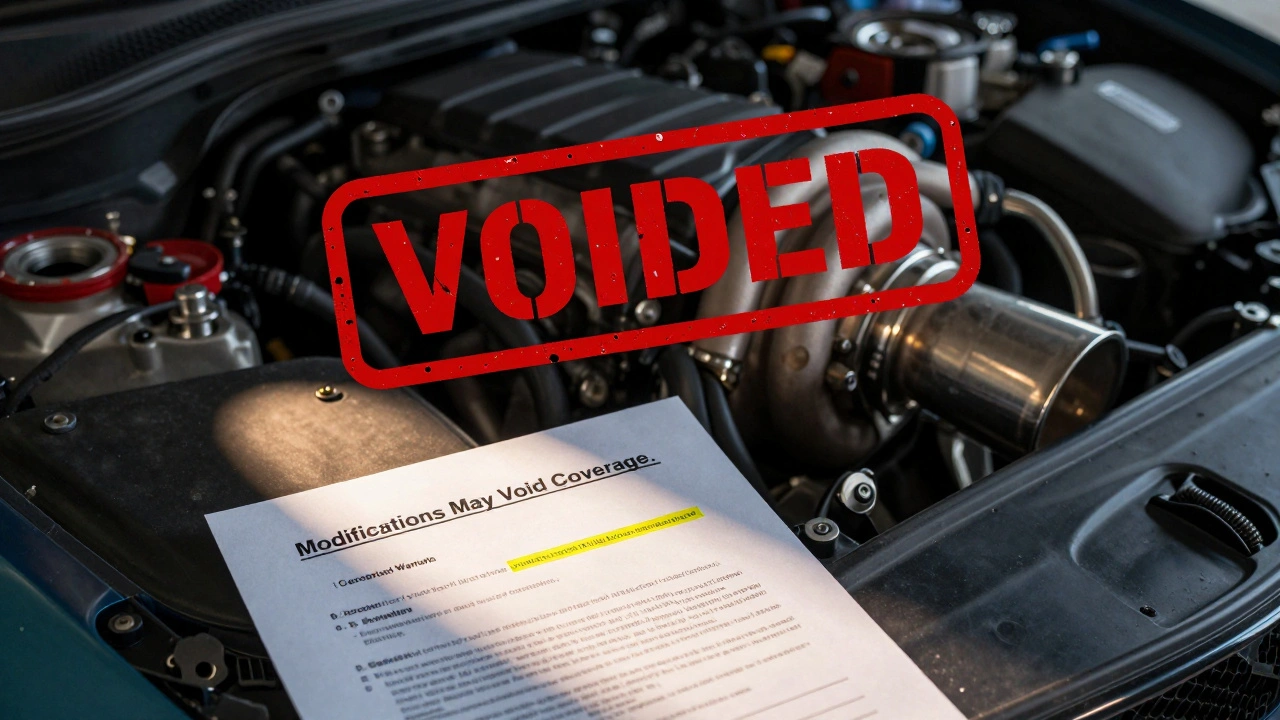

If your car had a leaky gasket, a noisy bearing, or a flickering dashboard light before you bought the warranty, that’s on you. Warranty companies will check your vehicle’s service history and sometimes even do a pre-purchase inspection. If they find evidence of a problem before your contract started, they’ll deny any claim related to it. That’s why getting a pre-buy inspection from a trusted mechanic is critical. Fix known issues before signing up - or you’ll be stuck with them.Aftermarket Parts Can Void Coverage

You put on a performance air intake, upgraded your exhaust, or added a custom stereo? That might sound cool, but it can cancel your warranty coverage - not just for the modified part, but for related systems too. For example, if you install a turbocharger and later the engine blows, the warranty company can deny the claim because the modification changed how the engine operates. Even using non-OEM parts like aftermarket brake pads can trigger exclusions if they cause damage to the calipers or rotors.Accidents, Theft, and Natural Disasters Don’t Count

Extended warranties are for mechanical breakdowns - not accidents. If you hit a tree, get stolen from, or your car is hit by hail, that’s your insurance’s job. Same goes for flooding, lightning strikes, or fire damage. These are called “Acts of God” exclusions, and they’re in every single contract. Don’t confuse your extended warranty with comprehensive auto insurance. They’re not the same thing.Rust and Corrosion? Usually Excluded

Rust on your fender? Peeling paint? Interior carpet wear from muddy boots? These are cosmetic or environmental issues. Most warranties won’t cover them unless the rust came from a factory defect - like a poorly sealed door hinge that caused water to pool inside the frame. Even then, you’ll need to prove it wasn’t caused by neglect, like not washing your car after driving on salted roads in winter. In places like Portland, where winter rain and road salt are common, rust claims are often denied unless you can show the corrosion started from inside the metal, not from surface exposure.

Negligence Can Void Everything

If you ignore the recommended service schedule - say, you go 15,000 miles between oil changes - the warranty company can void your entire contract. They don’t need to prove the neglect caused the failure. Just showing you didn’t follow the manual is enough. Same goes for using the wrong oil, ignoring warning lights, or driving with low coolant. These aren’t minor slips - they’re red flags. Warranty providers have the right to deny claims if your maintenance history looks sloppy.Consequential Damage Is Tricky

Here’s a common trap: Your transmission fails. That’s covered. But because it failed, it damaged the U-joint, the driveshaft, and the differential. Now you’re looking at $4,000 in repairs. Most extended warranties will only pay for the transmission - not the parts it broke. That’s called a “consequential damage exclusion.” Some premium plans, like Endurance’s Elite Benefits, do cover these secondary failures - but you have to read the fine print. Always ask: “Does this plan cover damage caused by the covered part?” If they hesitate, walk away.What You Should Do Before Buying

Don’t just compare prices. Compare exclusions. Here’s how:- Get the full contract in writing - no verbal promises.

- Read the exclusions section line by line. Highlight every item listed as not covered.

- Ask: “If my alternator dies, will this cover it?” If they say “probably,” ask for written confirmation.

- Check if they require inspections before claims. Some companies send inspectors to repair shops to verify when parts failed.

- Look for plans that include maintenance allowances or tire coverage - those add real value.

Bottom Line

An extended warranty isn’t magic. It’s a contract with limits. The best ones don’t promise everything - they clearly say what they’ll cover and what they won’t. If a company won’t give you a clear list of exclusions, walk away. The goal isn’t to buy the cheapest plan - it’s to buy the one that won’t leave you surprised when you need it most.Can I still use my extended warranty if I bought a used car?

Yes, most extended warranties are transferable and work on used cars - even ones with over 100,000 miles. Companies like Endurance cover vehicles up to 20 years old and 200,000 miles. But the key is the condition at the time of purchase. If the car had existing issues before you signed up, those won’t be covered. Always get a pre-purchase inspection and keep the report.

Do all extended warranties have the same exclusions?

No. While most exclude routine maintenance and wear-and-tear parts, the details vary. Some cover alternators; others don’t. Some include consequential damage; most don’t. One plan might cover rust from manufacturing defects; another won’t. Always compare exclusion lists side-by-side - not just prices.

What happens if I modify my car?

Modifications like performance chips, aftermarket exhausts, or lifted suspensions can void coverage on related systems. For example, a turbo upgrade might void engine coverage. Even non-performance changes - like a custom stereo or LED headlights - can be used as grounds to deny a claim if they’re linked to a failure. Always ask the warranty provider before installing anything.

Can I get my money back if I change my mind?

Most extended warranties offer a 30-day cancellation window with a full refund - as long as you haven’t filed a claim. After that, you might get a prorated refund based on time left and mileage. Always check the cancellation policy before signing. Some companies charge restocking fees or require you to pay for a vehicle inspection before refunding.

Is it worth buying an extended warranty for an older car?

It depends. If your car is reliable and you’re good at saving for repairs, skip it. But if you drive a high-mileage vehicle with expensive parts - like a luxury sedan with a complex transmission - an extended warranty can be worth it. For example, replacing a transmission on a 2018 Honda Accord costs $3,500+. If a $1,800 warranty plan covers it and you drive 15,000 miles a year, it pays for itself in one repair.